The 2018 Analyst Conference presentation was very informative in a number of areas. By the end of the day last Monday, investors had many reasons to feel good about Micron��s (NASDAQ:MU) future direction and relative priorities. One area that continued to be rather opaque, however, was information pertaining to the company��s plans for exploiting 3D XPoint technology (hereafter, XP). There were subtle clues, though, and this article will discuss what these clues portend for this potentially game-changing technology.

The information we did get from Micron��s presentation revealed a widening divergence with Intel (NASDAQ:INTC), and that is pretty much a continuation of a trend that began back in 2015 with their joint introduction of XP. Since that introduction, XP has been delayed by more than two years from its original timeline and beset with ongoing dire rumors regarding its technical and financial feasibility. Despite that, Intel has never ceased aggressively hyping the technology and its potential impact on the company's bottom line. Micron, on the other hand, has been almost completely silent, revealing little other than its branding - QuantX�� - and its confidence that the new memory has great potential.

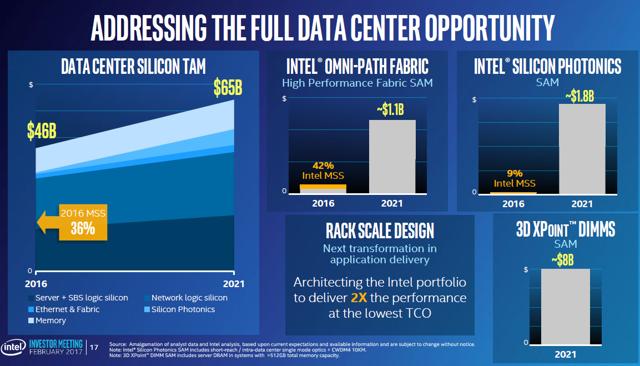

As of today, the two companies' positions could not be more starkly different. In its 2017 Investor Meeting, Intel projected up to $8 billion in XP DIMM revenue in 2021. I have attached the pertinent slide below:

Since then, Intel has announced that it will be shipping XP DIMMs in the second half of this year (CY 2018) and has doubled down on its XP manufacturing footprint in Lehi with the announcement in November 2017 of the completion of a large expansion of Building 60. What��s more, Micron announced in its Q2 earnings call that Intel loaned Micron the $500 million investment required of each of the partners in the buildout of XP production at Lehi. Pursuant to their IMFT agreement, this gives Intel to the right to more of the total share of XP production at Lehi unless/until Micron reimburses Intel at some point in the future.

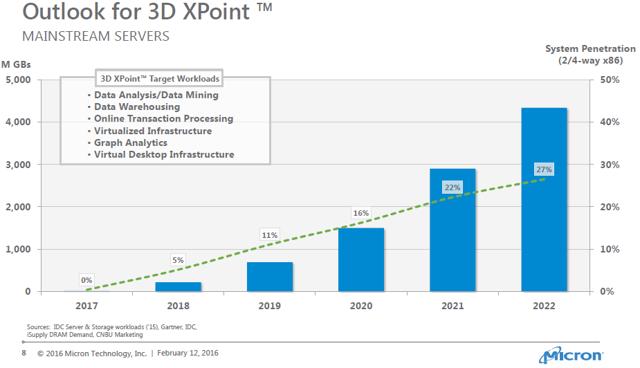

Micron, on the other hand, has been almost completely silent on any projections for XP beyond the February 2016 Analysts Conference which forecasts the following:

And now, as of last week��s Analyst Conference update, here is Sanjay Mehrotra setting expectations for the commercialization of XP:

��we will be having products in 3D XPoint in 2019, launching those products in the latter part of 2019 timeframe.��

And here is Sumit Sandana in his briefing positioning the new Micron XP products:

��[...] our customers are looking forward to using 3D XPoint to expand the foot print of memory inside their servers.��

And here is Scott DeBoer giving us the latest technology update:

��Right now, the 3D XPoint technology that we��re focused on is second generation technology and that��s now moved over into manufacturing. Again, [it] combined the performance and the density that we��ve talked about several times before and improves the cost structure with the second generation of technology.��

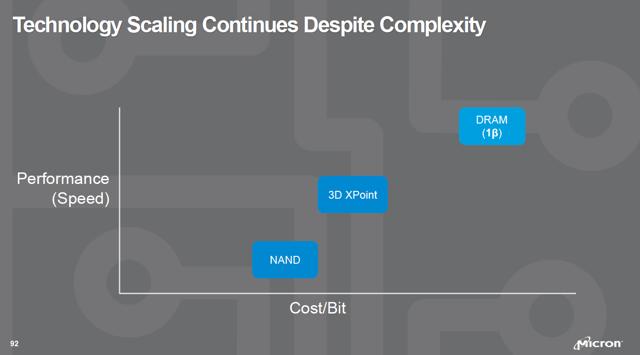

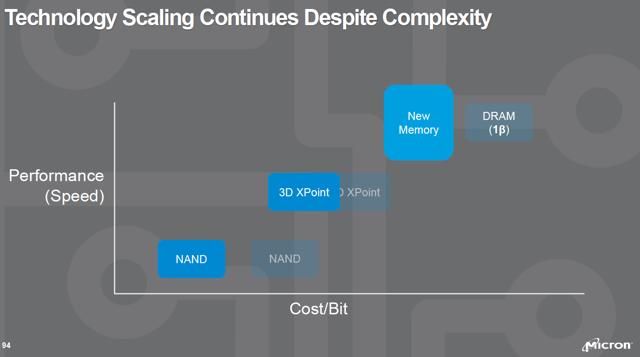

And the final bit of information we can glean about XP was depicted in three cryptic DeBoer slides that show Micron��s expectations regarding process advances in the technology in the future. The first slide shows the current relative position of the three technologies on the performance versus cost axis.

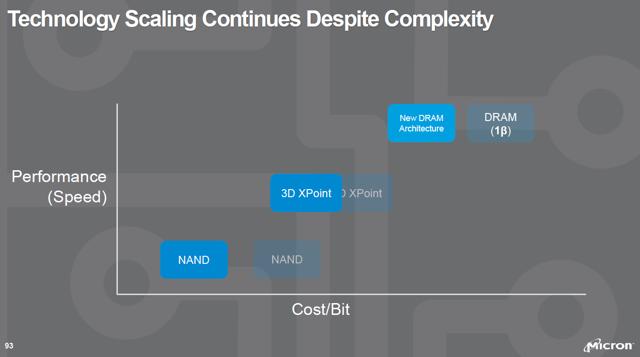

The second slide in the series shows the relative movement on the cost axis over time:

And the final slide shows the current perspective on the end points of the current technology road map and the emergence of a ��New Memory�� technology with DRAM-like performance and cost.

So, with the combination of the companies�� actions above, we see the two partners moving in opposite directions in regard to the technology. Intel is plunging in and doubling down, while Micron hangs back and, while positive about the future potential, downplays the technology in the short run. As it stands now, Intel, while not publicly forecasting material XP revenues in 2019, is obviously expecting that the launch of XP DIMMs will ignite the business and start the company on the ramp that will take it to that $8 billion number in CY 2021.

Micron, on the other hand, because of its August fiscal year end, will not see the first revenues from XP until its FY ��20, and has yet to provide an update to its 2016 slide projections. To further dampen short-term expectations, it has even speculated that the company would be selling its share of Lehi XP production to Intel in the near term. Here��s Dave Zinsner from the Q&A session of the Q2 earnings con call:

��So 3D crosspoint products are expected to come out in - sometime in calendar year 2019. We will have - sometimes we'll have underloading charges. It's possible that our partner might take some of the - of those wafers so that would obviously help on the underutilization.��

Is there a way to explain these seemingly opposite viewpoints about a technology that both partners agree is potentially revolutionary in its impact? I believe there is, and this explanation is congruent with the expectation that XP technology will be successful. Let��s get to it.

First off, let��s be clear as we can be about what Micron is telling us about XP. The three DeBoer slides above provide a lot of information about how Micron sees XP technology advancing. The first slide shows the relative positioning of the three technologies, NAND, XP, and DRAM on a log scale graph comparing speed versus cost per bit. We��re going to talk in more detail about Micron��s DRAM roadmap in a moment, but for now, all we need to focus on is the relative positioning. Basically, XP is shown to be slightly more expensive than NAND, but is significantly faster.

Before we go further, we must remember that in the semiconductor world, the terms density and cost are interchangeable. So does Micron think that XP will increase in density over the next few years? Slide 2 answers that question in the affirmative. Note how the XP cost/bit band moves to a position almost directly over today��s NAND. That is a remarkable statement and very bullish for the future of the technology. With today��s current generation of NAND costing roughly $.10/GB, the opportunity for Micron and Intel to be extremely profitable with XP is obvious - if the density of XP can achieve the gains DeBoer is depicting, either by adding layers or by shrinking the die lithography from its current 20nm level to possibly as low as 7nm over time.

To be clear, the timing of these denser (and thus, less costly) XP technology generations is very fuzzy. If we use the DRAM generation, 1尾, as our guideline, that��s four shrinks out from this year��s 1X - 1Y, 1Z, 1伪, and finally, 1尾. So, 1尾 could be anywhere from four to six years out. The point is that these slides demonstrate that Micron clearly thinks that XP will be economic at some point, and it may give us a clue as to why Intel and Micron decided to end their NAND partnership at IM.

We know now what Micron��s NAND plans are. The company is going to charge trap technology for the Gen 4 node that will follow the last IM node, the 96-layer die. Given that the 64L technology just got to bit crossover in the last two months, that means it will be the dominant node all through 2019, leaving Gen 3 to fiscal years 2020 through 2021 in which it will be fully productive and cost-effective. Given that cadence, Micron will probably be introducing CT Gen 4 sometime in 2021 in anticipation of full production sometime in FY 2022.

Is it possible that Intel feels it doesn��t need another NAND node because it can increase XP densities enough to be an attractive alternative to NAND? We don��t know for sure, because Intel has not announced its post Gen 3 roadmap. We do have clarity on Micron��s position, though. The company is confident that the CT-based 3D NAND technology has the potential to advance to 200+ layers, and that means NAND will remain the economic choice for storage architectures well into the mid-20��s, if not longer.

Let��s pause for a moment here to recap. Here��s what we know or can infer:

Intel and Micron are parting ways on NAND. The last IM node, the Gen 3 96L die, will be highly competitive, if not market-leading, in cost through FY 2020 and much of FY 2021. Intel is planning for $8 billion of XP revenue in CY 2021. Micron won��t see any revenue from XP until its FY ��20. Micron has ceded much of its XP output from Lehi to Intel, at least until it pays back the $500 million loan from Intel used to fund the Building 60 expansion at Lehi. Micron has announced a DRAM technology roadmap that has four generations beyond the current ��1X�� node. Intel has not announced its post-Gen 3 3D NAND technology roadmap. Micron��s recent analyst meeting technology futures slides indicate that the company thinks that XP will get significantly more dense over the course of the next four to six years.

So what can Micron investors take away from all this? Here��s my take on it, for what it��s worth:

Micron has concluded that DRAM has at least a four to six-year runway, whether XP is successful or not. The company feels it has a viable business in 3D NAND over the foreseeable future (well into the mid-2020��s). The company thinks that it can have a viable XP business in FY ��20 and beyond, but has not characterized the size or potential scope of that business. Micron thinks that XP has a serious potential to impact the growth of the DRAM business by the mid-2020��s.

Of the above, point #1 is the key to Micron��s business results through FY 2021. Micron will remain a DRAM company and will rise (or fall) depending on the health of the DRAM market. If I had to speculate about Micron��s current strategic outlook, my view is that the company sees the DRAM business at this point as a reliably growing cash cow that can be depended on for the foreseeable future. The company does feel that XP will be viable, and at some point XP will potentially impact DRAM demand - but that time is four to five years away at the earliest.

A skeptic could challenge my position by asking - if Micron is so bullish on DRAM, why has it not announced a new DRAM fab? To which I would answer:

That would be the wrong signal to send to the Koreans regarding industry capacity management. Micron probably feels that such a fab - which, if it were to be announced at the upcoming Q3 earnings call, would not be in full production until 2020 - would have some or all of its capacity stranded by 2025, when it is still not fully through its 7-year depreciation cycle. The company is going to need its CapEx dollars to either build its own or contribute to another IM XP fab in the 2020 time frame.

In closing, my take on this is that Micron��s opacity on XP becomes much less opaque when we understand the implications of the company's announcement that it sees at least four more DRAM generations in its development plans. Whatever happens with XP in the short term, the DRAM market will remain robust and highly profitable, driving Micron��s profits and cash flow into record-setting territory over the course of the next few years. Intel may or may not succeed in the short term, but its success or lack thereof will have no material effect on Micron. Over the longer term, post 2020, Micron is poised to win big with XP once Intel has done all the pioneering work establishing the market. Heads (XP fails or is slow in market development) Micron wins, tails (XP is a big success) it wins bigger.

Remember, I say Micron, you say DRAM - for the next few years, at any rate.

Long MU.

Disclosure: I am/we are long MU, NVDA, WDC, PSTG.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Xiaomi CEO Lei Jun at the Hong Kong stock exchange on Monday.

Xiaomi CEO Lei Jun at the Hong Kong stock exchange on Monday.

Pillar (CURRENCY:PLR) traded 4.8% higher against the US dollar during the one day period ending at 22:00 PM ET on July 4th. In the last week, Pillar has traded 0.1% higher against the US dollar. Pillar has a total market capitalization of $39.03 million and approximately $42,674.00 worth of Pillar was traded on exchanges in the last day. One Pillar token can currently be purchased for about $0.15 or 0.00002279 BTC on popular cryptocurrency exchanges including Cryptopia, Bancor Network, EtherDelta (ForkDelta) and HitBTC.

Pillar (CURRENCY:PLR) traded 4.8% higher against the US dollar during the one day period ending at 22:00 PM ET on July 4th. In the last week, Pillar has traded 0.1% higher against the US dollar. Pillar has a total market capitalization of $39.03 million and approximately $42,674.00 worth of Pillar was traded on exchanges in the last day. One Pillar token can currently be purchased for about $0.15 or 0.00002279 BTC on popular cryptocurrency exchanges including Cryptopia, Bancor Network, EtherDelta (ForkDelta) and HitBTC.

Cavalier Investments LLC lifted its stake in shares of Consumer Discretionary SPDR (NYSEARCA:XLY) by 67.9% in the first quarter, according to the company in its most recent disclosure with the SEC. The institutional investor owned 184,419 shares of the exchange traded fund’s stock after buying an additional 74,598 shares during the quarter. Consumer Discretionary SPDR makes up approximately 6.6% of Cavalier Investments LLC’s portfolio, making the stock its 5th biggest position. Cavalier Investments LLC owned 0.15% of Consumer Discretionary SPDR worth $18,680,000 at the end of the most recent reporting period.

Cavalier Investments LLC lifted its stake in shares of Consumer Discretionary SPDR (NYSEARCA:XLY) by 67.9% in the first quarter, according to the company in its most recent disclosure with the SEC. The institutional investor owned 184,419 shares of the exchange traded fund’s stock after buying an additional 74,598 shares during the quarter. Consumer Discretionary SPDR makes up approximately 6.6% of Cavalier Investments LLC’s portfolio, making the stock its 5th biggest position. Cavalier Investments LLC owned 0.15% of Consumer Discretionary SPDR worth $18,680,000 at the end of the most recent reporting period.